It’s inevitable that every company must be out there battling for market share, but you don’t really want to be in a situation where the competition is so stiff that any potential upside is eroded away in the process—―a scenario known as perfect competition in economics. To avoid perfect competition, companies must strive to build an economic moat that gives them a sustainable competitive advantage over time. While these protective moats can arise from a number of different sources, in today’s information economy they most often arise from the power of innovation. But where does innovation come from, and is there a universal framework that can be applied to help consistently make big breakthroughs?

The 10 Types of Innovation

In today’s infographic, we showcase the culmination of years of in-depth research from Doblin, an innovation-focused firm now owned by Deloitte. After examining over 2,000 business innovations throughout history, Doblin uncovered that most breakthroughs don’t necessarily stem from engineering inventions or rare discoveries. Instead, they observed that innovations can be categorized within a range of 10 distinct dimensions—and anyone can use the resulting strategic framework to analyze the competition, to stress test for product weaknesses, or to find new opportunities for their products. Here are the 10 types of innovation:

From Theory to Practice

What does innovation look like in practice? Let’s see how well-known businesses have leveraged each of these 10 types of innovation in the past, while also diving into the tactics that modern businesses can use to consistently make new product breakthroughs:.

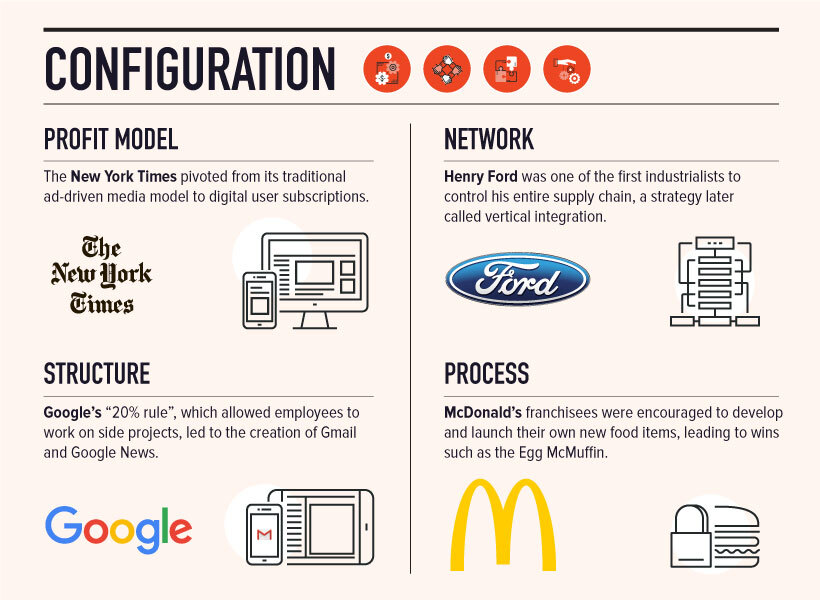

Innovation Types #1-4: “Configuration”

According to Doblin, the first four types of innovation center around the configuration of the company, and all the work that happens “behind the scenes”. Although innovation types in this category are not directly customer-facing, as you can see in the examples below, they can still have an important impact on the customer experience. How your company and products are organized can have a crucial downstream effect, even enabling innovations in other categories.

Two of the most interesting examples here are Google and McDonald’s. Both companies made internal innovations that empowered their people to make important advancements further on downstream. In the case of McDonald’s, the franchisee insight that led to the introduction of the Egg McMuffin spearheaded the company’s entire breakfast offering, which now accounts for 25% of revenues. Breakfast is also now the company’s most profitable segment.

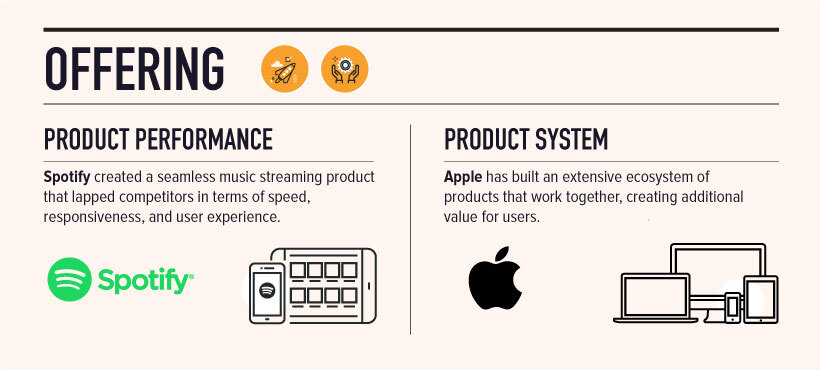

Innovation Types #5-6: “Offering”

When most people think of innovation, it’s likely the offering category that comes to mind. Making improvements to product performance is an obvious but difficult type of innovation, and unless it’s accompanied by a deeply ingrained company culture towards technical innovation, such advancements may only create a temporary advantage against the competition. This is the part of the reason that Doblin recommends that companies focus on combining multiple areas of innovation together—it creates a much more stable economic moat.

Apple has a reputation for innovation, but the product ecosystem highlighted above is an underappreciated piece of the company’s strategy. By putting thought into the ecosystem of products—and ensuring they work together flawlessly—additional utility is created, while also making it harder for customers to switch away from Apple products.

Innovation Types #7-10: “Experience”

These types of innovation are the most customer-facing, but this also makes them the most subject to interpretation. While other innovations tend to occur upstream, innovations in experience all get trialed in the hands of customers. For this reason, intense care is needed in rolling out these ideas.

Executing on such a promise was no small task, but today there are 150 million users of Prime worldwide, including some in metro areas who can get items in as little as two hours.

Making Innovations Happen in Your Organization

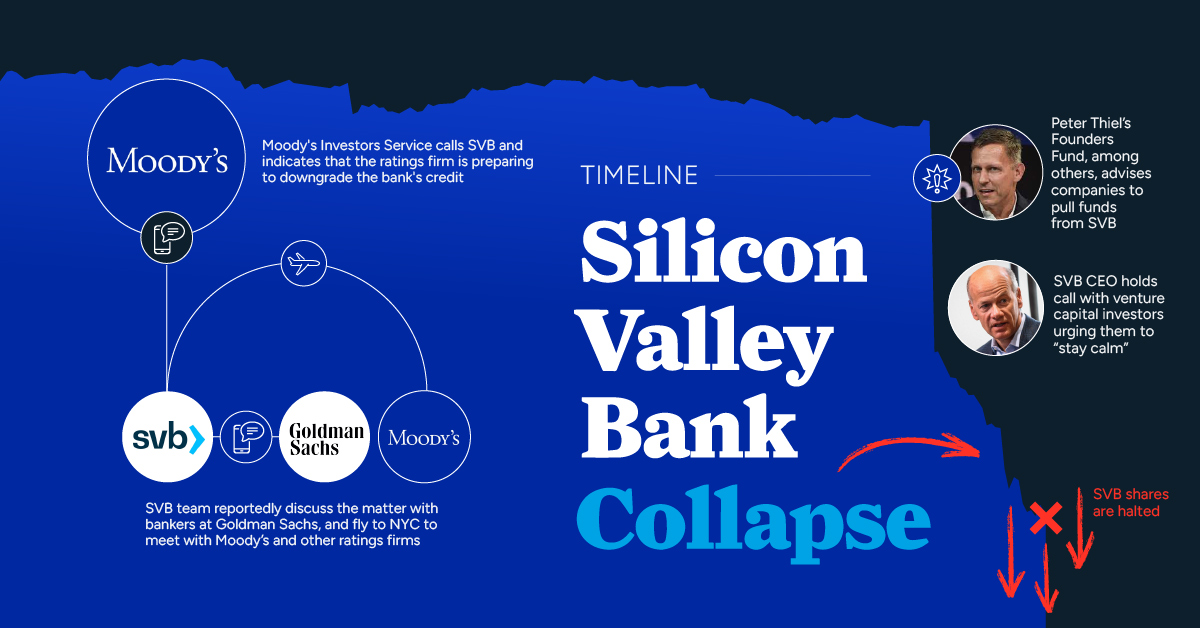

How can organizations approach the 10 types of innovation from a more tactical perspective? One useful resource is Doblin’s free public list of over 100 tactics that correspond with the aforementioned framework. The one-pager PDF provides a range of typical dimensions for approaching each type of innovation. In essence, these are all different ways you could consider when trying to differentiate your product or service—and at the very least, it provides a useful thought experiment for managers and marketers. For those interested in learning more on this topic, Doblin also has a highly-rated book as well as other accessories that leverage the above framework. on But fast forward to the end of last week, and SVB was shuttered by regulators after a panic-induced bank run. So, how exactly did this happen? We dig in below.

Road to a Bank Run

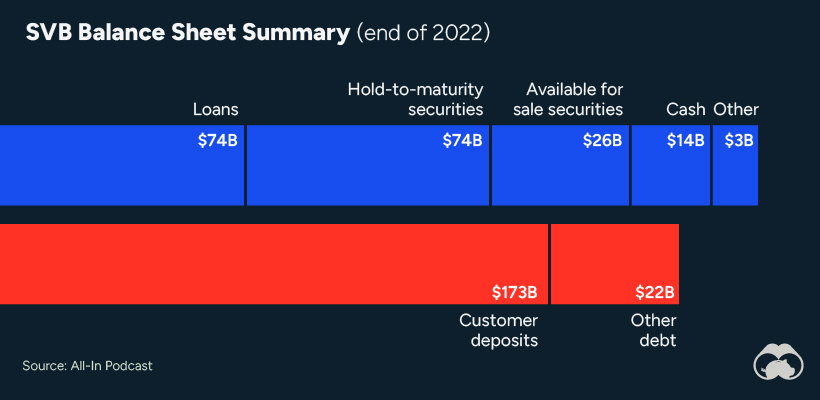

SVB and its customers generally thrived during the low interest rate era, but as rates rose, SVB found itself more exposed to risk than a typical bank. Even so, at the end of 2022, the bank’s balance sheet showed no cause for alarm.

As well, the bank was viewed positively in a number of places. Most Wall Street analyst ratings were overwhelmingly positive on the bank’s stock, and Forbes had just added the bank to its Financial All-Stars list. Outward signs of trouble emerged on Wednesday, March 8th, when SVB surprised investors with news that the bank needed to raise more than $2 billion to shore up its balance sheet. The reaction from prominent venture capitalists was not positive, with Coatue Management, Union Square Ventures, and Peter Thiel’s Founders Fund moving to limit exposure to the 40-year-old bank. The influence of these firms is believed to have added fuel to the fire, and a bank run ensued. Also influencing decision making was the fact that SVB had the highest percentage of uninsured domestic deposits of all big banks. These totaled nearly $152 billion, or about 97% of all deposits. By the end of the day, customers had tried to withdraw $42 billion in deposits.

What Triggered the SVB Collapse?

While the collapse of SVB took place over the course of 44 hours, its roots trace back to the early pandemic years. In 2021, U.S. venture capital-backed companies raised a record $330 billion—double the amount seen in 2020. At the time, interest rates were at rock-bottom levels to help buoy the economy. Matt Levine sums up the situation well: “When interest rates are low everywhere, a dollar in 20 years is about as good as a dollar today, so a startup whose business model is “we will lose money for a decade building artificial intelligence, and then rake in lots of money in the far future” sounds pretty good. When interest rates are higher, a dollar today is better than a dollar tomorrow, so investors want cash flows. When interest rates were low for a long time, and suddenly become high, all the money that was rushing to your customers is suddenly cut off.” Source: Pitchbook Why is this important? During this time, SVB received billions of dollars from these venture-backed clients. In one year alone, their deposits increased 100%. They took these funds and invested them in longer-term bonds. As a result, this created a dangerous trap as the company expected rates would remain low. During this time, SVB invested in bonds at the top of the market. As interest rates rose higher and bond prices declined, SVB started taking major losses on their long-term bond holdings.

Losses Fueling a Liquidity Crunch

When SVB reported its fourth quarter results in early 2023, Moody’s Investor Service, a credit rating agency took notice. In early March, it said that SVB was at high risk for a downgrade due to its significant unrealized losses. In response, SVB looked to sell $2 billion of its investments at a loss to help boost liquidity for its struggling balance sheet. Soon, more hedge funds and venture investors realized SVB could be on thin ice. Depositors withdrew funds in droves, spurring a liquidity squeeze and prompting California regulators and the FDIC to step in and shut down the bank.

What Happens Now?

While much of SVB’s activity was focused on the tech sector, the bank’s shocking collapse has rattled a financial sector that is already on edge.

The four biggest U.S. banks lost a combined $52 billion the day before the SVB collapse. On Friday, other banking stocks saw double-digit drops, including Signature Bank (-23%), First Republic (-15%), and Silvergate Capital (-11%).

Source: Morningstar Direct. *Represents March 9 data, trading halted on March 10.

When the dust settles, it’s hard to predict the ripple effects that will emerge from this dramatic event. For investors, the Secretary of the Treasury Janet Yellen announced confidence in the banking system remaining resilient, noting that regulators have the proper tools in response to the issue.

But others have seen trouble brewing as far back as 2020 (or earlier) when commercial banking assets were skyrocketing and banks were buying bonds when rates were low.