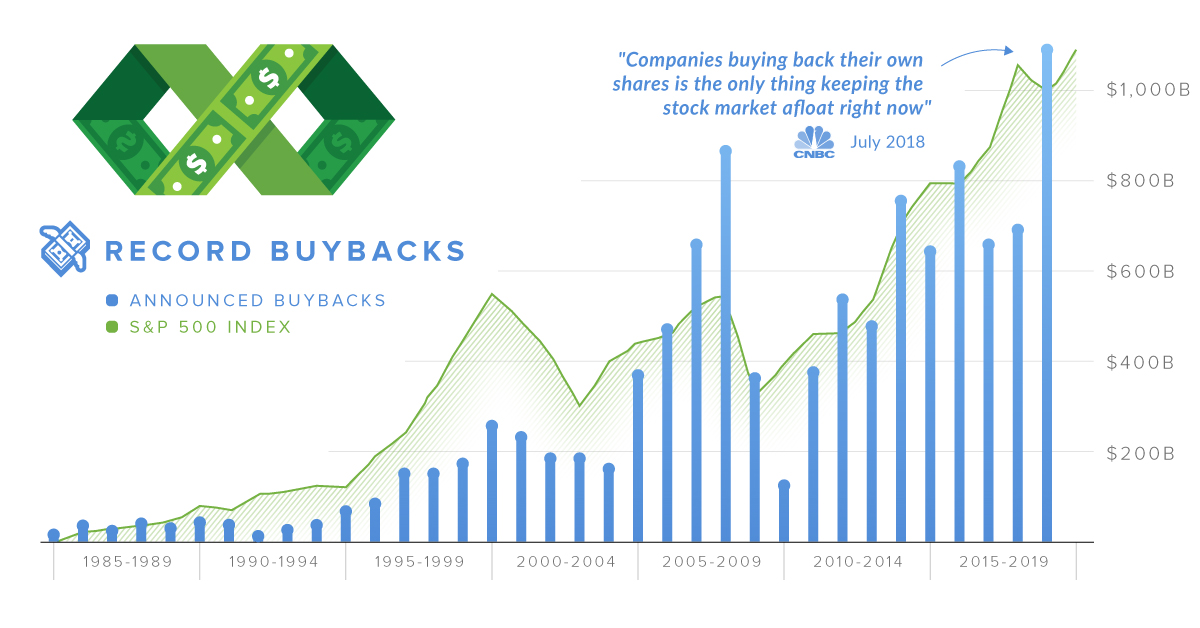

But as soon as trillions of dollars are being poured into any single cause – regardless of how innocuous it may sound – there is always the potential to make a lightning rod for controversy. With stock buybacks totaling $1.1 trillion in 2018, they’re at the center of discussion more than ever before.

What are Stock Buybacks?

When publicly-traded companies want to return money to shareholders, they generally have two options. The first is to declare a dividend, but the other is to repurchase its own shares on the open market. Although it seems meta, stock buybacks are a way for companies to re-invest in themselves. Each buyback decreases the amount of shares outstanding, with the company re-absorbing the portion of ownership that was previously distributed among investors. In other words, buybacks are somewhat analogous to buying out a business partner – they allow the remaining partners to own a higher share of the company.

Pro vs. Con

With the amount of stock buybacks rising to historic highs, they have been front and center in 2019. Here are what proponents and opponents are arguing about. Pro Case: Proponents of buybacks say that if they are done rationally, buybacks (like dividends) are just another way to return cash to shareholders. Stock prices for companies that have bought back shares are also higher, in general, than other companies on major indices like the S&P 500. Con Case: Opponents of stock buybacks say that they increase inequality, and that executives make short-term oriented decisions around buybacks that allow them to maximize personal gain. In other words, when a company probably should be investing in its people or its business, the company is instead giving money back to the wealthy owners – and only they benefit.

The Bottom Line

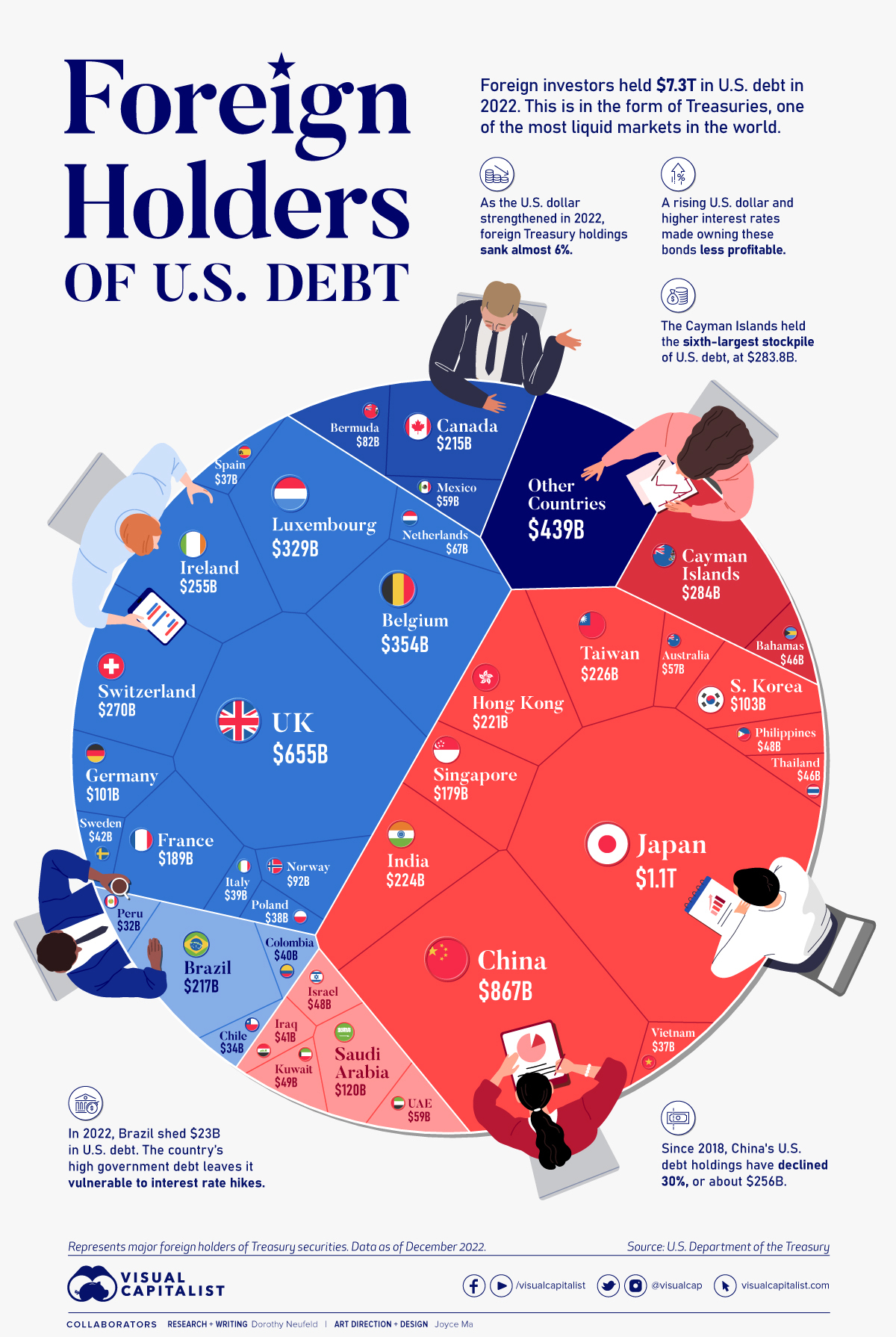

While both sides make a compelling argument for different reasons, the only real way to evaluate stock buybacks is based on the merits of individual companies. If the company is returning money to shareholders because it is the best allocation of capital, then it can make perfect sense. If the company is doing it at the expense of growing its business and the wages of employees, one can see why stock buybacks may rub people the wrong way. on These are in the form of Treasury securities, some of the most liquid assets worldwide. Central banks use them for foreign exchange reserves and private investors flock to them during flights to safety thanks to their perceived low default risk. Beyond these reasons, foreign investors may buy Treasuries as a store of value. They are often used as collateral during certain international trade transactions, or countries can use them to help manage exchange rate policy. For example, countries may buy Treasuries to protect their currency’s exchange rate from speculation. In the above graphic, we show the foreign holders of the U.S. national debt using data from the U.S. Department of the Treasury.

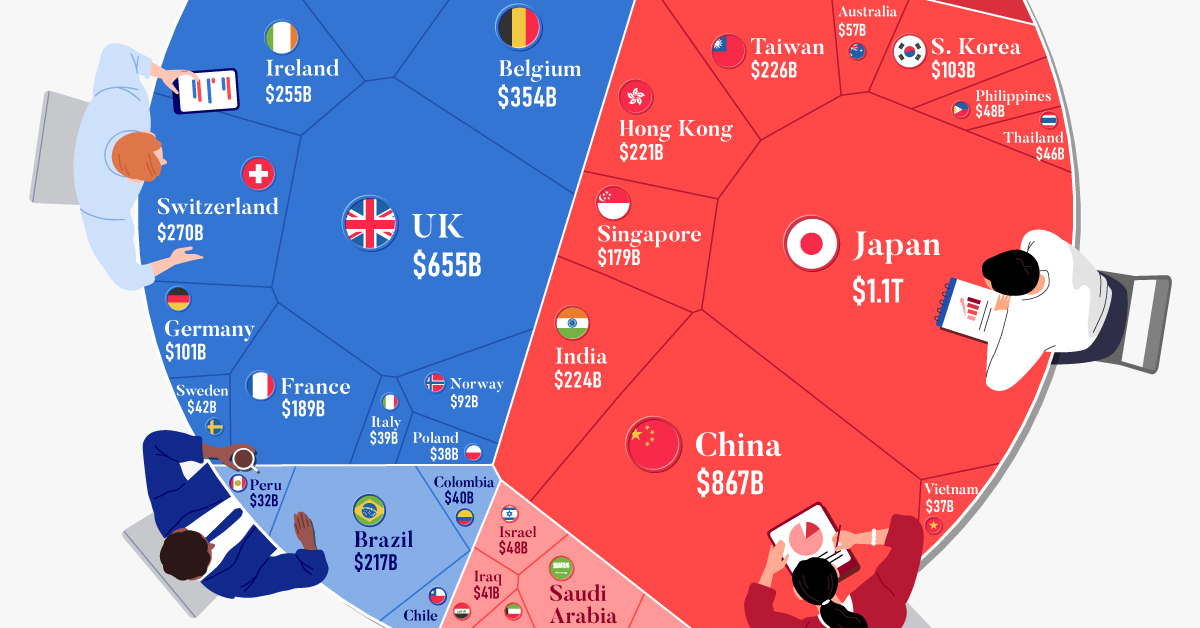

Top Foreign Holders of U.S. Debt

With $1.1 trillion in Treasury holdings, Japan is the largest foreign holder of U.S. debt. Japan surpassed China as the top holder in 2019 as China shed over $250 billion, or 30% of its holdings in four years. This bond offloading by China is the one way the country can manage the yuan’s exchange rate. This is because if it sells dollars, it can buy the yuan when the currency falls. At the same time, China doesn’t solely use the dollar to manage its currency—it now uses a basket of currencies. Here are the countries that hold the most U.S. debt: As the above table shows, the United Kingdom is the third highest holder, at over $655 billion in Treasuries. Across Europe, 13 countries are notable holders of these securities, the highest in any region, followed by Asia-Pacific at 11 different holders. A handful of small nations own a surprising amount of U.S. debt. With a population of 70,000, the Cayman Islands own a towering amount of Treasury bonds to the tune of $284 billion. There are more hedge funds domiciled in the Cayman Islands per capita than any other nation worldwide. In fact, the four smallest nations in the visualization above—Cayman Islands, Bermuda, Bahamas, and Luxembourg—have a combined population of just 1.2 million people, but own a staggering $741 billion in Treasuries.

Interest Rates and Treasury Market Dynamics

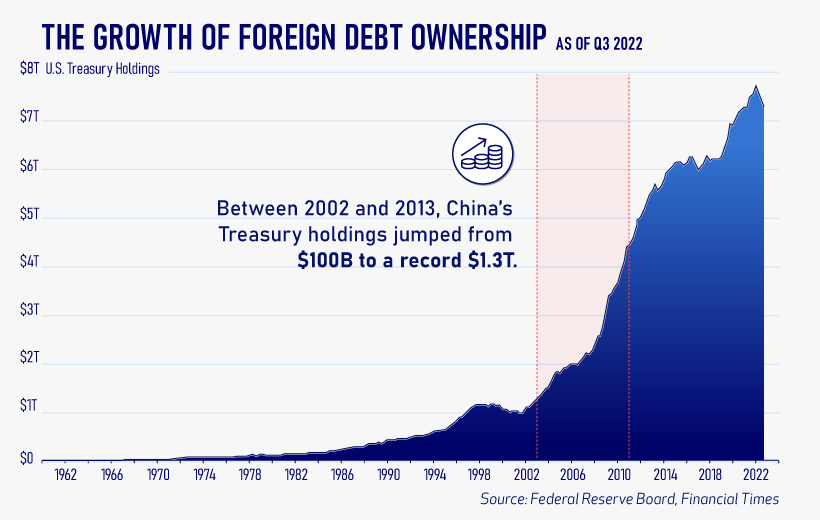

Over 2022, foreign demand for Treasuries sank 6% as higher interest rates and a strong U.S. dollar made owning these bonds less profitable. This is because rising interest rates on U.S. debt makes the present value of their future income payments lower. Meanwhile, their prices also fall. As the chart below shows, this drop in demand is a sharp reversal from 2018-2020, when demand jumped as interest rates hovered at historic lows. A similar trend took place in the decade after the 2008-09 financial crisis when U.S. debt holdings effectively tripled from $2 to $6 trillion.

Driving this trend was China’s rapid purchase of Treasuries, which ballooned from $100 billion in 2002 to a peak of $1.3 trillion in 2013. As the country’s exports and output expanded, it sold yuan and bought dollars to help alleviate exchange rate pressure on its currency. Fast-forward to today, and global interest-rate uncertainty—which in turn can impact national currency valuations and therefore demand for Treasuries—continues to be a factor impacting the future direction of foreign U.S. debt holdings.