Despite the volatility, the combination of the Federal Reserve’s early stimulus interventions and positive vaccine news has rewarded dip-buyers and strong hands. Along with visualizing the returns across asset classes, currencies, and S&P 500 sectors, we’ve included their maximum drawdown for the year—the drop from the 2020 open to the 2020 lows—along with the recovery from 2020 lows to the closing price. This helps visualize 2020’s most resilient assets, along with the strength of their recovery.

Markets Roundup for 2020

Of all the major asset classes, precious metals provided the best returns last year.

Gold finished the year up 24.6%, but down from its all-time highs of $2,075/oz achieved on August 7th. Gold was also a resilient asset. Thanks to its strong start in January (4.8%), when March came around gold held up and only fell 4.4% below the yearly open. Silver’s performance over the year was also sterling, offering investors 47.4% returns despite a -34.7% pullback in March.

Here’s a look at how all major asset classes performed over the course of the year: U.S. equities and emerging market equities had double-digit returns despite the tumultuous year. Small cap stocks in the Russell 2000 outpaced the S&P 500 by 3%, but also saw a steeper drawdown during times of volatility. Although there were some wild drawdowns in 2020, nothing compared to the drop into negative prices for WTI crude oil that occurred in April. Futures traded all the way down to -$37.63 a barrel when travel cancellations brought oil demand to a standstill and supply cut agreements weren’t reached by OPEC members. U.S. government and corporate bonds had a positive year, however their returns were primarily driven by support from the Federal Reserve’s monetary policy and market operations. The Federal Reserve increased its portfolio of Treasury notes and bonds by 79% since March, with its total assets reaching $7.3 trillion at the end of 2020.

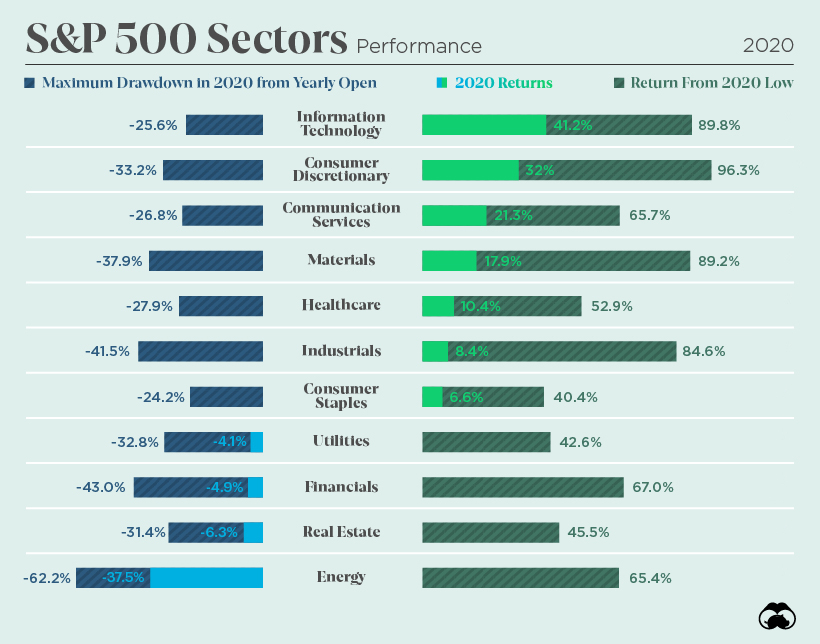

Performance by S&P 500 Sector

Unsurprisingly, the energy sector was hit the hardest last year, with value sectors generally struggling to perform compared to growth sectors.

As the communication services (21.3%) and consumer discretionary (32%) sectors also performed well, the latter saw the biggest bounce from the lows of any S&P 500 sector (96%).

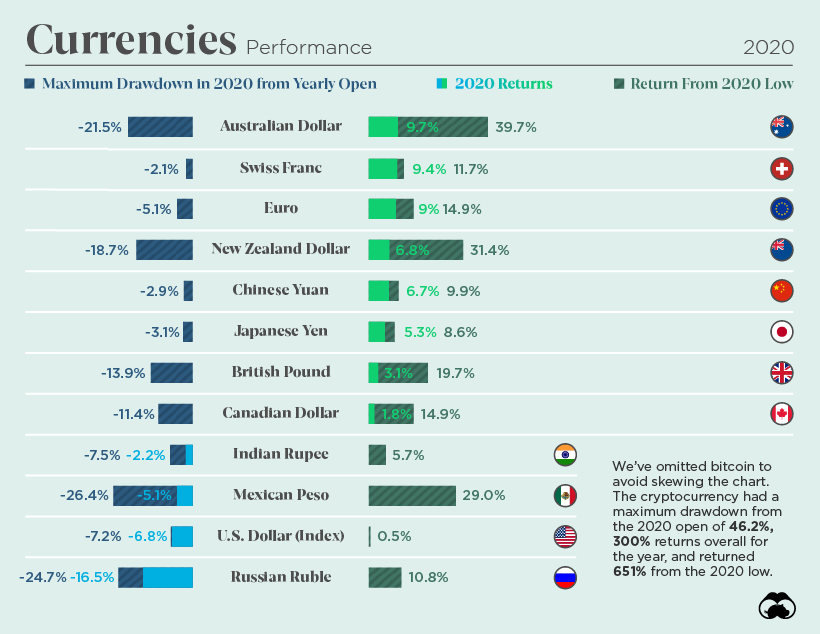

Foreign Exchange Performance in 2020

Early on in the year, major currencies generally followed similar patterns as they all fell against the U.S. dollar in March’s flight to safety. The Swiss franc was one of the most resilient currencies, drawing down only -2.1% from the 2020 open. It was also one of the best performers at the end of the year alongside the euro and Australian dollar with gains of 9% or more.

Timing the dip on the Australian or New Zealand dollar was the most rewarding opportunity for forex traders last year. Meanwhile, the Indian rupee, Mexican peso, and Russian ruble weren’t able to claw back the points they lost in March, with the ruble seeing double-digit losses. All eyes have been on the U.S. dollar’s free-fall downwards since it spiked up in March, and as the Biden administration prepares to take office, speculative traders have returned to selling dollars.

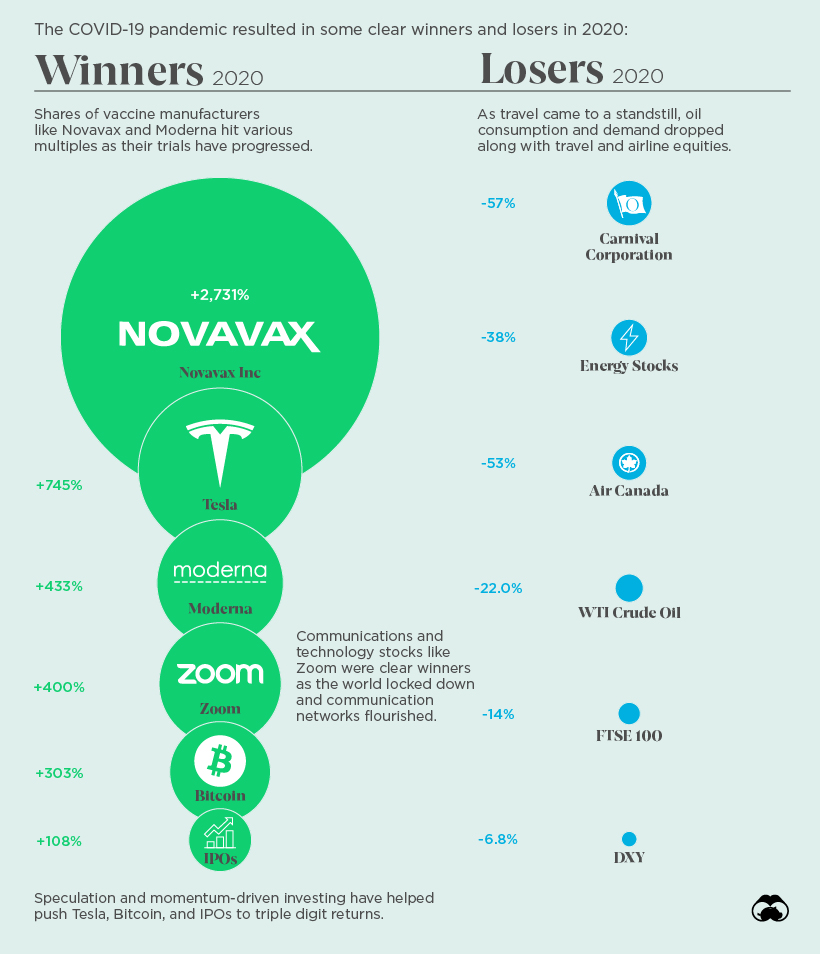

Winners and Losers of 2020

The COVID-19 pandemic largely defined many of the winners and losers of 2020, as did the Federal Reserve’s expansion of the U.S. money supply. Zoom became an essential communications service in lockdown and Moderna and Novavax shares skyrocketed in valuation as they announced their COVID-19 vaccines.

Bitcoin broke well beyond its previous all-time high, returning just over 300% from the 2020 open and more than 650% from the lows. Tesla had an even more spectacular run, returning 745% and making Elon Musk the second-richest man in the world. Meanwhile, as global travel quickly came to a halt last year, Carnival Corporation (the world’s biggest cruise operator) and Air Canada suffered double-digit losses along with WTI crude oil and much of the energy sector and travel industry. Vaccine rollouts and the U.S. stimulus bill are the current known-unknowns that the market is pricing in for this upcoming year, and investors will be watching to see if the dollar’s downturn will be reversed, or if the world’s major reserve currency will continue to decline in 2021. on Last year, stock and bond returns tumbled after the Federal Reserve hiked interest rates at the fastest speed in 40 years. It was the first time in decades that both asset classes posted negative annual investment returns in tandem. Over four decades, this has happened 2.4% of the time across any 12-month rolling period. To look at how various stock and bond asset allocations have performed over history—and their broader correlations—the above graphic charts their best, worst, and average returns, using data from Vanguard.

How Has Asset Allocation Impacted Returns?

Based on data between 1926 and 2019, the table below looks at the spectrum of market returns of different asset allocations:

We can see that a portfolio made entirely of stocks returned 10.3% on average, the highest across all asset allocations. Of course, this came with wider return variance, hitting an annual low of -43% and a high of 54%.

A traditional 60/40 portfolio—which has lost its luster in recent years as low interest rates have led to lower bond returns—saw an average historical return of 8.8%. As interest rates have climbed in recent years, this may widen its appeal once again as bond returns may rise.

Meanwhile, a 100% bond portfolio averaged 5.3% in annual returns over the period. Bonds typically serve as a hedge against portfolio losses thanks to their typically negative historical correlation to stocks.

A Closer Look at Historical Correlations

To understand how 2022 was an outlier in terms of asset correlations we can look at the graphic below:

The last time stocks and bonds moved together in a negative direction was in 1969. At the time, inflation was accelerating and the Fed was hiking interest rates to cool rising costs. In fact, historically, when inflation surges, stocks and bonds have often moved in similar directions. Underscoring this divergence is real interest rate volatility. When real interest rates are a driving force in the market, as we have seen in the last year, it hurts both stock and bond returns. This is because higher interest rates can reduce the future cash flows of these investments. Adding another layer is the level of risk appetite among investors. When the economic outlook is uncertain and interest rate volatility is high, investors are more likely to take risk off their portfolios and demand higher returns for taking on higher risk. This can push down equity and bond prices. On the other hand, if the economic outlook is positive, investors may be willing to take on more risk, in turn potentially boosting equity prices.

Current Investment Returns in Context

Today, financial markets are seeing sharp swings as the ripple effects of higher interest rates are sinking in. For investors, historical data provides insight on long-term asset allocation trends. Over the last century, cycles of high interest rates have come and gone. Both equity and bond investment returns have been resilient for investors who stay the course.