There are several reasons for this crisis and the economic turmoil has sparked mass protests and violence across the country. This visual breaks down some of the elements that led to Sri Lanka’s current situation.

A Timeline of Events

The ongoing problems in Sri Lanka have bubbled up after years of economic mismanagement. Here’s a brief timeline looking at just some of the recent factors.

2009

In 2009, a decades-long civil war in the country ended and the government’s focus turned inward towards domestic production. However, a stress on local production and sales, instead of exports, increased the reliance on foreign goods.

2019

Unprompted cuts were introduced on income tax in 2019, leading to significant losses in government revenue, draining an already cash-strapped country.

2020

The COVID-19 pandemic hit the world causing border closures globally and stifling one of Sri Lanka’s most lucrative industries. Prior to the pandemic, in 2018, tourism contributed nearly 5% of the country’s GDP and generated over 388,000 jobs. In 2020, tourism’s share of GDP had dropped to 0.8%, with over 40,000 jobs lost to that point.

2021

Recently, the Sri Lankan government introduced a ban on foreign-made chemical fertilizers. The ban was meant to counter the depletion of the country’s foreign currency reserves. However, with only local, organic fertilizers available to farmers, a massive crop failure occurred and Sri Lankans were subsequently forced to rely even more heavily on imports, further depleting reserves.

April 2022

In early April this year, massive protests calling for President Gotabaya Rajapaksa’s resignation, sparked in Sri Lanka’s capital city, Colombo.

May 2022

In May, pro-government supporters brutally attacked protesters. Subsequently, Prime Minister Mahinda Rajapaksa, brother of President Rajapaksa, stepped down and was replaced with former PM, Ranil Wickremesinghe.

June 2022

Recently, the government approved a four-day work week to allow citizens an extra day to grow food, as prices continue to shoot up. Food inflation increased over 57% in May. Additionally, the increasing prices on grain caused by the war in Ukraine and rising fuel prices globally have played into an already dire situation in Sri Lanka.

The Key Information

One of the main causes of the economic crisis in Sri Lanka is the reliance on imports and the amount spent on them. Let’s take a look at the numbers:

2021 total imports = $20.6 billion USD 2022 total imports (to March) = $5.7 billion USD

In contrast, the most recent reported foreign currency reserve levels in the country were at an abysmal $50 million, having plummeted an astounding 99%, from $7.6 billion in 2019. Some of the top imports in 2021, according to the country’s central bank were:

Refined petroleum = $2.8 billion Textiles = $3.1 billion Chemical products = $1.1 billion Food & beverage = $1.7 billion

Of course, without the cash to purchase these goods from abroad, Sri Lankans face an increasingly drastic situation. Additionally, the debt Sri Lanka has incurred is huge, further hampering their ability to boost their reserves. Recently, they defaulted on a $78 million loan from international creditors, and in total, they’ve borrowed $50.7 billion. The largest source of their debt is by far due to market borrowings, followed closely by loans taken from the Asian Development Bank, China, and Japan, among others.

What it Means

Sri Lanka is home to more than 22 million people who are rapidly losing the ability to purchase everyday goods. Consumer inflation reached 39% at the end of May. Due to power outages meant to save energy and fuel, schools are currently shuttered and children have nowhere to go during the day. Protesters calling for the president’s resignation have been camped in the capital for months, facing tear gas from police and backlash from president Rajapaksa’s supporters, but many have also responded violently to pushback. India and China have agreed to send help to the country and the the International Monetary Fund recently arrived in the country to discuss a bailout. Additionally, the government has sent ministers to Russia to discuss a deal for discounted oil imports.

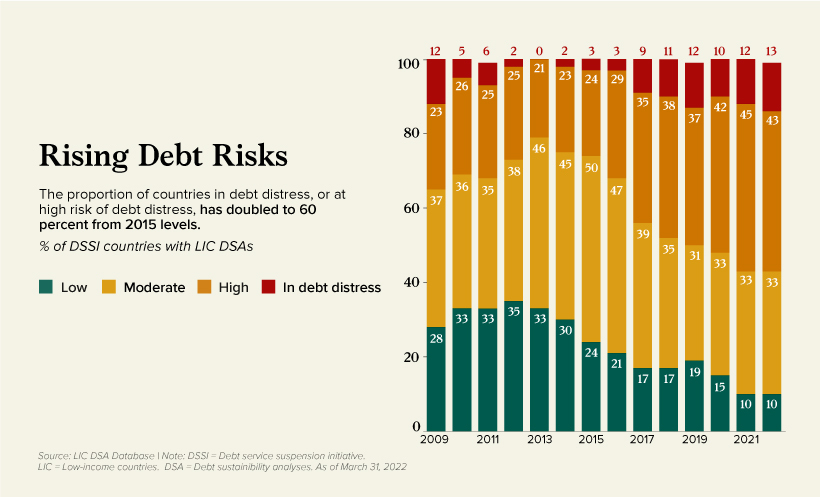

A Foreshadowing for Low Income Countries

Governments need foreign currency in order to purchase goods from abroad. Without the ability to purchase or borrow foreign currency, the Sri Lankan government cannot buy desperately needed imports, including food staples and fuel, causing domestic prices to rise. Furthermore, defaults on loan payments discourage foreign direct investment and devalue the national currency, making future borrowing more difficult. What’s happening in Sri Lanka may be an ominous preview of what’s to come in other low and middle-income countries, as the risk of debt distress continues to rise globally. The Debt Service Suspension Initiative (DSSI) was implemented by G20 countries, suspending nearly $13 billion in debt from the start of the pandemic until late 2021.

Some DSSI and LIC countries facing a high risk of debt distress include Zambia, Ethiopia, and Tajikistan, to name a few. Going forward, Sri Lanka’s next steps in managing this situation will either serve as a useful example for other countries at risk or a warning worth heeding.

Ongoing Updates

Since this article was published the situation has changed significantly in Sri Lanka. Protesters have received their original demand calling for president Rajapaksa to step down — both he and prime minister Wickremesinghe have agreed to resign. This comes after protesters stormed the president’s palace causing him to flee the country. Note: The debt breakdown in the main visualization represents total outstanding external debt owed to foreign creditors rather total debt. on Last year, stock and bond returns tumbled after the Federal Reserve hiked interest rates at the fastest speed in 40 years. It was the first time in decades that both asset classes posted negative annual investment returns in tandem. Over four decades, this has happened 2.4% of the time across any 12-month rolling period. To look at how various stock and bond asset allocations have performed over history—and their broader correlations—the above graphic charts their best, worst, and average returns, using data from Vanguard.

How Has Asset Allocation Impacted Returns?

Based on data between 1926 and 2019, the table below looks at the spectrum of market returns of different asset allocations:

We can see that a portfolio made entirely of stocks returned 10.3% on average, the highest across all asset allocations. Of course, this came with wider return variance, hitting an annual low of -43% and a high of 54%.

A traditional 60/40 portfolio—which has lost its luster in recent years as low interest rates have led to lower bond returns—saw an average historical return of 8.8%. As interest rates have climbed in recent years, this may widen its appeal once again as bond returns may rise.

Meanwhile, a 100% bond portfolio averaged 5.3% in annual returns over the period. Bonds typically serve as a hedge against portfolio losses thanks to their typically negative historical correlation to stocks.

A Closer Look at Historical Correlations

To understand how 2022 was an outlier in terms of asset correlations we can look at the graphic below:

The last time stocks and bonds moved together in a negative direction was in 1969. At the time, inflation was accelerating and the Fed was hiking interest rates to cool rising costs. In fact, historically, when inflation surges, stocks and bonds have often moved in similar directions. Underscoring this divergence is real interest rate volatility. When real interest rates are a driving force in the market, as we have seen in the last year, it hurts both stock and bond returns. This is because higher interest rates can reduce the future cash flows of these investments. Adding another layer is the level of risk appetite among investors. When the economic outlook is uncertain and interest rate volatility is high, investors are more likely to take risk off their portfolios and demand higher returns for taking on higher risk. This can push down equity and bond prices. On the other hand, if the economic outlook is positive, investors may be willing to take on more risk, in turn potentially boosting equity prices.

Current Investment Returns in Context

Today, financial markets are seeing sharp swings as the ripple effects of higher interest rates are sinking in. For investors, historical data provides insight on long-term asset allocation trends. Over the last century, cycles of high interest rates have come and gone. Both equity and bond investment returns have been resilient for investors who stay the course.