Presented by: Nevada Energy Metals, eCobalt Solutions Inc., and Great Lakes Graphite

Introduction to The Battery Series

Today, how we store energy is just as important as how we create it. Battery technology already makes electric cars possible, as well as helping us to store emergency power, fly satellites, and use portable electronic devices. But tomorrow, could you be boarding a battery-powered airplane, or living in a city powered at night by solar energy? The Battery Series is a five-part infographic series that explores how batteries work, the players in the market, the materials needed to build batteries, and how future battery developments may affect the world. This is Part 1, which looks at the basics of batteries and the history of battery technology.

Battery Basics

Batteries convert stored chemical energy directly into electrical energy. Batteries have three main components: (-) Anode:The negative electrode that gets oxidized, releasing electrons (+) Cathode: The positive electrode that is reduced, by acquiring electrons Electrolyte: The medium that provides the ion transport mechanism between the cathode and anode of a cell. It can be liquid or solid. At the most basic level, batteries are very simple. In fact, a primitive battery can even be made with a copper penny, galvanized nail (zinc), and a lemon or potato.

The Evolution of Battery Technology

While creating a simple battery is quite easy, the challenge is that making a good battery is very difficult. Balancing power, weight, cost, and other factors involves managing many trade-offs, and scientists have worked for hundreds of years to get to today’s level of efficiency. Here’s a brief history of how batteries have changed over the years: Voltaic Pile (1799) Italian physicist Alessandro Volta, in 1799, created the first electrical battery that could provide continuous electrical current to a circuit. The voltaic pile used zinc and copper for electrodes with brine-soaked paper for an electrolyte. His invention disproved the common theory that electricity could only be created by living beings. Daniell Cell (1836) About 40 years later, a British chemist named John Frederic Daniell would create a new cell that would solve the “hydrogen bubble” problem of the Voltaic pile. This previous problem, in which bubbles collected on the bottom of the zinc electrodes, limited the pile’s lifespan and uses. The Daniell cell, invented in 1836, used a copper pot filled with copper sulfate solution, which was further immersed in an earthenware container filled with sulfuric acid and a zinc electrode. The Daniell cell’s electrical potential became the basis unit for voltage, equal to one volt. Lead-acid (1859) The lead-acid battery was the first rechargeable battery, invented in 1859 by French physicist Gaston Planté. Lead-acid batteries excel in two areas: they are very low cost, and they also can supply high surge currents. This makes them suitable for automobile starter motors even with today’s technology, and it’s part of the reason $44.7 billion of lead-acid batteries were sold globally in 2014. Nickel Cadmium (1899) NiCd batteries were invented in 1899 by Waldemar Jungner in Sweden. The first ones were “wet-cells” similar to lead-acid batteries, using a liquid electrolyte. Nickel Cadmium batteries helped pave the way for modern technology, but they are being used less and less because of cadmium’s toxicity. NiCd batteries lost 80% of their market share in the 1990s to batteries that are more familiar to us today. Alkaline Batteries (1950s) Popularized by brands like Duracell and Energizer, alkaline batteries are used in regular household devices from remote controls to flashlights. They are inexpensive and typically non-rechargeable, though they can be made rechargeable by using a specially designed cell. The modern alkaline battery was invented by Canadian engineer Lewis Urry in the 1950s. Using zinc and manganese oxide in the electrodes, the battery type gets its name from the alkaline electrolyte used: potassium hydroxide. Over 10 billion alkaline batteries have been made in the world. Nickel-Metal Hydride (1989) Similar to the rechargeable NiCd battery, the NiMH formulation uses a hydrogen-absorbing alloy instead of toxic cadmium. This makes it more environmentally safe – and it also helps to increase the energy density. NiMH batteries are used in power tools, digital cameras, and some other electronic devices. They also were used in early hybrid vehicles such as the Toyota Prius. The development of the NiMH spanned two decades, and was sponsored by Daimler-Benz and Volkswagen AG. The first commercially available cells were in 1989. Lithium-Ion (1991) Sony released the first commercial lithium-ion battery in 1991. Lithium-ion batteries have high energy density and have a number of specific cathode formulations for different applications. For example, lithium cobalt dioxide (LiCoO2) cathodes are used in laptops and smartphones, while lithium nickel cobalt aluminum oxide (LiNiCoAlO2) cathodes, also known as NCAs, are used in the batteries of vehicles such as the Tesla Model S. Graphite is a common material for use in the anode, and the electrolyte is most often a type of lithium salt suspended in an organic solvent.

The Rechargeable Battery Spectrum

There are several factors that could affect battery choice, including cost. However, here are two of the most important factors that determine the fit and use of rechargeable batteries specifically: Think of specific energy as in the amount of water in a tank. It’s the amount of energy a battery holds in total. Meanwhile, specific power is the speed at which that water can pour out of the tank. It’s the amount of current a battery can supply for a given use. And while today the lithium-ion battery is the workhorse for gadgets and electric vehicles – what batteries will be vital to our future? How big is that market? Find out in the rest of the Battery Series. (Parts 2 through 5 will be released throughout the summer of 2016).

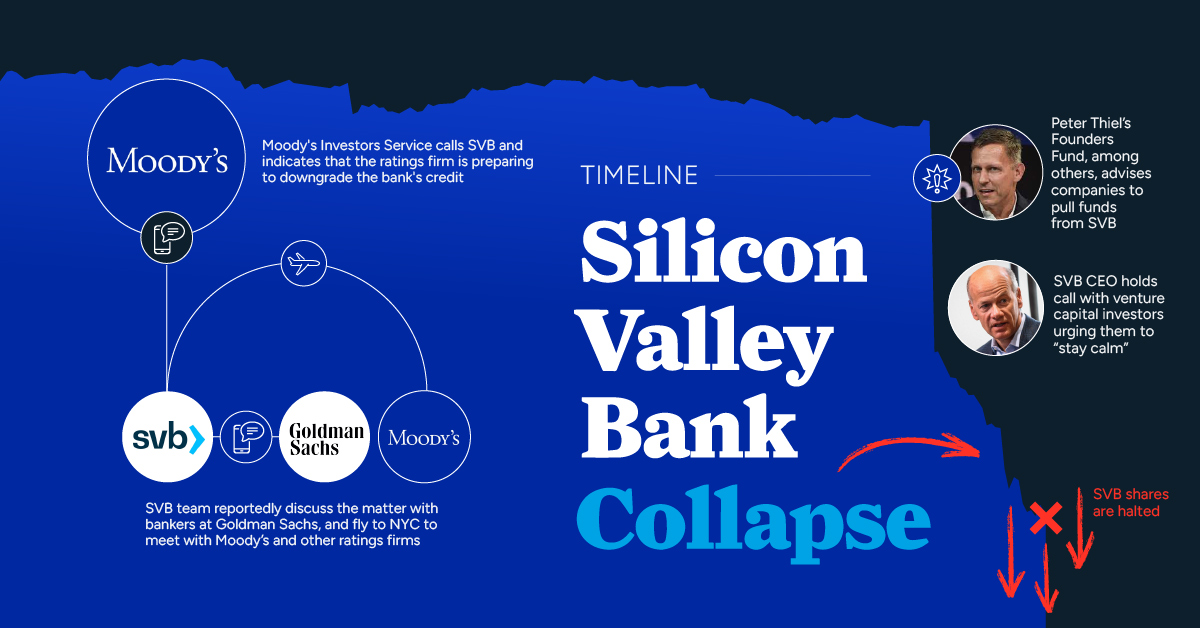

on But fast forward to the end of last week, and SVB was shuttered by regulators after a panic-induced bank run. So, how exactly did this happen? We dig in below.

Road to a Bank Run

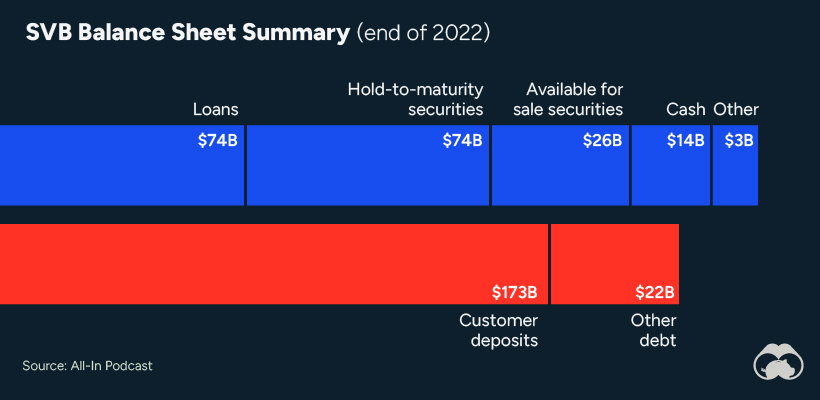

SVB and its customers generally thrived during the low interest rate era, but as rates rose, SVB found itself more exposed to risk than a typical bank. Even so, at the end of 2022, the bank’s balance sheet showed no cause for alarm.

As well, the bank was viewed positively in a number of places. Most Wall Street analyst ratings were overwhelmingly positive on the bank’s stock, and Forbes had just added the bank to its Financial All-Stars list. Outward signs of trouble emerged on Wednesday, March 8th, when SVB surprised investors with news that the bank needed to raise more than $2 billion to shore up its balance sheet. The reaction from prominent venture capitalists was not positive, with Coatue Management, Union Square Ventures, and Peter Thiel’s Founders Fund moving to limit exposure to the 40-year-old bank. The influence of these firms is believed to have added fuel to the fire, and a bank run ensued. Also influencing decision making was the fact that SVB had the highest percentage of uninsured domestic deposits of all big banks. These totaled nearly $152 billion, or about 97% of all deposits. By the end of the day, customers had tried to withdraw $42 billion in deposits.

What Triggered the SVB Collapse?

While the collapse of SVB took place over the course of 44 hours, its roots trace back to the early pandemic years. In 2021, U.S. venture capital-backed companies raised a record $330 billion—double the amount seen in 2020. At the time, interest rates were at rock-bottom levels to help buoy the economy. Matt Levine sums up the situation well: “When interest rates are low everywhere, a dollar in 20 years is about as good as a dollar today, so a startup whose business model is “we will lose money for a decade building artificial intelligence, and then rake in lots of money in the far future” sounds pretty good. When interest rates are higher, a dollar today is better than a dollar tomorrow, so investors want cash flows. When interest rates were low for a long time, and suddenly become high, all the money that was rushing to your customers is suddenly cut off.” Source: Pitchbook Why is this important? During this time, SVB received billions of dollars from these venture-backed clients. In one year alone, their deposits increased 100%. They took these funds and invested them in longer-term bonds. As a result, this created a dangerous trap as the company expected rates would remain low. During this time, SVB invested in bonds at the top of the market. As interest rates rose higher and bond prices declined, SVB started taking major losses on their long-term bond holdings.

Losses Fueling a Liquidity Crunch

When SVB reported its fourth quarter results in early 2023, Moody’s Investor Service, a credit rating agency took notice. In early March, it said that SVB was at high risk for a downgrade due to its significant unrealized losses. In response, SVB looked to sell $2 billion of its investments at a loss to help boost liquidity for its struggling balance sheet. Soon, more hedge funds and venture investors realized SVB could be on thin ice. Depositors withdrew funds in droves, spurring a liquidity squeeze and prompting California regulators and the FDIC to step in and shut down the bank.

What Happens Now?

While much of SVB’s activity was focused on the tech sector, the bank’s shocking collapse has rattled a financial sector that is already on edge.

The four biggest U.S. banks lost a combined $52 billion the day before the SVB collapse. On Friday, other banking stocks saw double-digit drops, including Signature Bank (-23%), First Republic (-15%), and Silvergate Capital (-11%).

Source: Morningstar Direct. *Represents March 9 data, trading halted on March 10.

When the dust settles, it’s hard to predict the ripple effects that will emerge from this dramatic event. For investors, the Secretary of the Treasury Janet Yellen announced confidence in the banking system remaining resilient, noting that regulators have the proper tools in response to the issue.

But others have seen trouble brewing as far back as 2020 (or earlier) when commercial banking assets were skyrocketing and banks were buying bonds when rates were low.